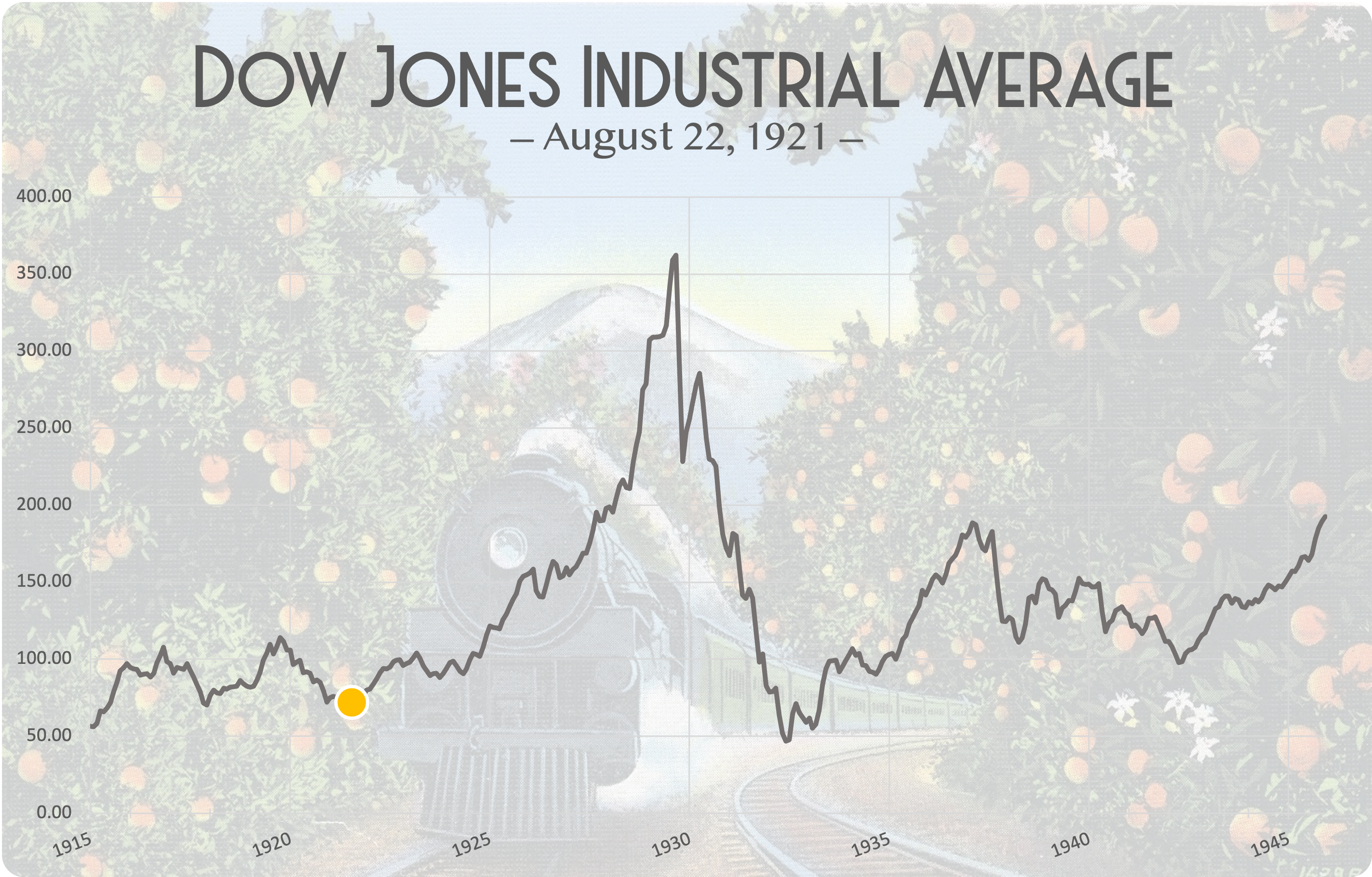

August 22-28, 1921

This week, the Dow Jones Industrial Average bottoms and the most notorious bull market in history begins.

Quick Stats:

DJIA: 64.52 (Today: 35,120)

Shiller PE Ratio: 5.2 (Today: 38.6)

Federal Reserve Bank of NY Discount Rate: 5.5% (Today: 0.25%)

GBPUSD: $3.64 (Today: $1.36)

Price of The Wall Street Journal: $0.07 (Today: $4.00)

Market-Moving Themes:

Stocks remain sluggish in the face of extreme value and rate cut rumors (equity, debt markets)

Raw material (sugar, oil, rubber, etc.) prices continue easing as wartime shortages abate (commodity markets)

German reparations hang over foreign exchange (currency markets)

Executive Summary:

Debt offerings are all the rage. Railroad debt. Public utility debt. Mortgage debt. There are opinion articles about the “reach” for yield, noting that 6-7% is possible from smaller companies. The day before the Dow takes its last leg down, the WSJ editors recommend pushing into the corporate debt periphery. They mention the 1870-1890 deflationary period as a potential template for the 1920s. Lower costs of living mean that one can live comfortably with modest income from bonds.

On Thursday, August 26, 1921, the WSJ front page ‘Review and Outlook’ section discusses letters they have received regarding the stock market averages making a fresh low on Tuesday. The editors mention many readers attach more weight to weakness than strength when stocks and commodities drop, and that the recent price movements may mean nothing at all.

Historical Fact: This is a special moment in history! Unbeknownst to market participants, the Dow Jones has bottomed. No bullish sentiment existed towards equities in 1921. The consensus has been wrong many times during major asset price inflection points. Think real estate in 2007 or stocks in 2009. For example, on the March 9, 2009 bottom, the WSJ published “Dow 5000? There's a Case for It.”

There is conversation on both sides of the pond regarding why stocks are declining in the face of positive business news. Equities and commodities are retracing back to post-war (1918) levels. Some continue to point out continued high taxation are hurting equities. Money that left equities during the war may re-enter under a lower tax regime, another writes. Nevertheless, terms such as "drifted back, "dispirited state" and "bearish tendency" emanate from equity and commodity prices.

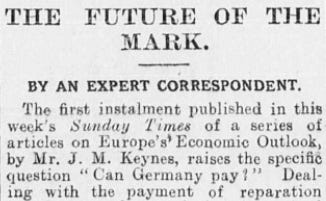

Germany’s situation is heating up. In an article titled “Can Germany pay?” by John Maynard Keynes, which was published in the Sunday Times on August 22, 1921, the Financial Times editors summarize his view in three points: (1) Germany will be able to make monthly reparation installments until May 1922, (2) undertaxation, particularly around brandy and agricultural products, are contributing to lower than possible revenue, and (3) it’s foolish for London analysts to recommend German 3% bonds when the prospect of default is only a couple years away. Keynes eerily suggests populist movements may void reparations due to increasing bitterness from German citizens.

August 24, 1921 - Financial Times Oil prices slid about 8% on Wednesday across New York and London markets. All gains over the past couple years have now been wiped away (oil trades for $25/barrel in 2021 dollars, down from $50/barrel one year prior). An article mentions a “flushing out” and “liquidation” originating from brokerage accounts in Scotland and Amsterdam. While crude oil price quotes display about two dozen flavors, the two common brands mentioned in 1921 are owned by Royal Dutch Shell (‘Shells’ and ‘Mexican Eagles’).

August 22, 1921 - Financial Times

Reading this newsletter is free. If you enjoy it, then please share to a friend or donate via PayPal (button below). You may also follow us on Twitter.