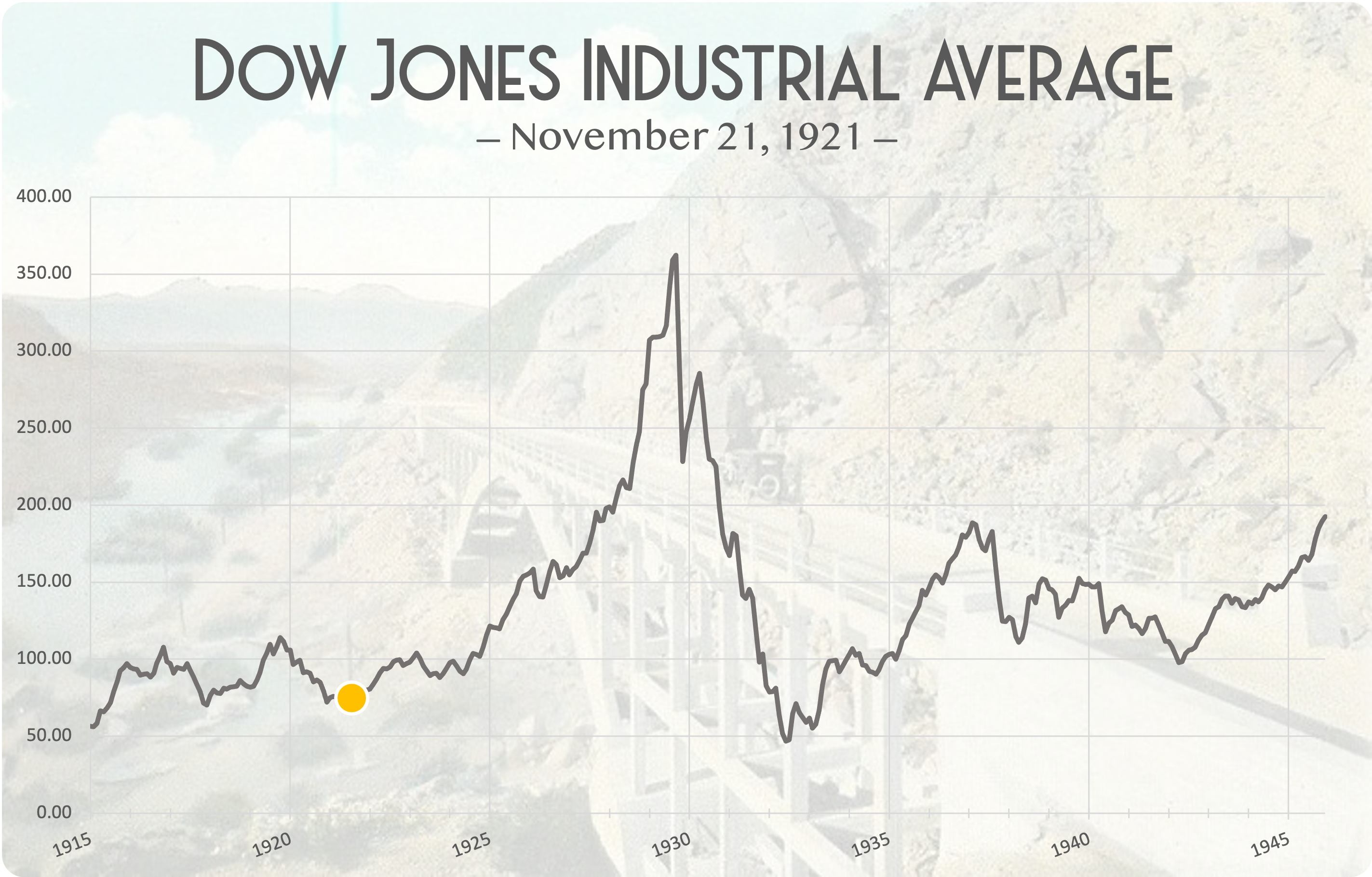

November 21-27, 1921

November 21-27, 1921

This week, the Revenue Act of 1921 becomes law and receives a muted response from investors.

Quick Stats:

DJIA: 77.31 (Today: 35,602)

Shiller PE Ratio: 5.9 (Today: 39.6)

Federal Reserve Bank of NY Discount Rate: 4.5% (Today: 0.25%)

GBPUSD: $3.99 (Today: $1.34)

Price of The Wall Street Journal: $0.07 (Today: $4.00)

Market-Moving Themes:

Sentiment slowly turning positive as business activity improves and financial conditions ease (equity, debt markets)

Wartime raw material shortages are ending, paving way for price stability (commodity markets)

European post-war debt payments are causing a strong dollar as gold flows to the United States (currency markets)

Executive Summary:

Stocks meander in a circle this week as traders and investors prepare for the Thanksgiving holiday. The worst of the market gyrations don’t feel over, so traders are hesitant to embrace the upward trend. As markets look ahead to 1922, fear and trepidation loom large. Paltry forecasts from last week blanket the papers.

Historical Fact: Today, the tendency for stocks to rally as they surmount negative news is known as “climbing a wall of worry.” As we approach 1922, this is exactly what’s happening. The late John Kenneth Galbraith once said, “the only function of economic forecasting is to make astrology look respectable.”

The feeling around the Revenue Act of 1921 is that nothing worthwhile has been accomplished. Some taxes have been eliminated or reduced, but not the most burdensome ones on businesses. The precise results from this Act will remain unknown for a few years, the article states, and Wall Street has yet to draw coherent and intelligent meanings from the bill. Treasury Secretary Andrew Mellon warmly embraces the news of passage.

Historical Fact: The Act of 1921 was the first of four pieces of legislation targeting personal income tax. While the media panned the 1921 one, Revenue Acts in 1924, 1926, and 1928 were more heroic. The top marginal income tax rate of the 1920s slid from 73% to 25% from 1920 to 1928, turbocharging consumer spending and swelling personal savings.

November 26, 1921 - The Wall Street Journal

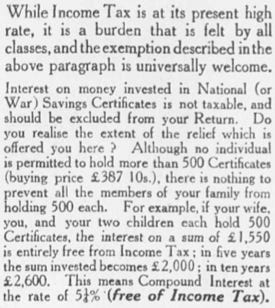

Onerous World War I-era income taxes pushed American and British investors into high quality bonds because accumulated interest was not taxable. Prominent financiers, like Otto Kahn, reiterated their recommendation for bond ownership many times in the press throughout 1920 and 1921. The FT features a piece on reasons why investors should stick with bonds.

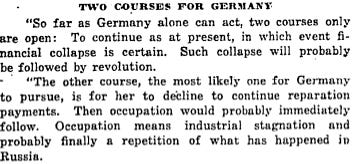

November 23, 1921 - Financial Times The dithering over Germany’s situation continues. This time, James Simpson, a VP for Marshall Field's (today known as Macy’s), writes to the Journal regarding his trip to Europe. What he finds shocks him: economic and financial chaos. He concludes Germany has two paths, and it will be up to the United States to arrest either from happening. The better path forward, in his view, is to provide 2-3 years of breathing room coupled with debt reductions to the current untenable reality.

November 23, 1921 - The Wall Street Journal

Reading this newsletter is free. If you enjoy it, then please share to a friend or donate via PayPal (button below). You may also follow us on Twitter.